Rhode Island has enacted a new tax commonly referred to as a “Taylor Swift Tax,” aimed at raising revenue from non-primary residences. The law targets certain second homes that are not rented for at least 183 days during the year, meaning that some owners of vacation properties—including long-held family cottages—could face thousands of dollars in additional annual costs even if their homes are modest. Several media reports say the measure is creating financial strain for families who rely on these properties as intergenerational assets, and some homeowners are considering legal challenges. Critics, including real estate groups, argue that the legislation’s financial impact and the process for its adoption have not been adequately explained or made transparent. Supporters point to the broader policy goal of addressing housing and revenue concerns, and comparisons are being made to other jurisdictions that have considered higher rates for second homes. Bloomberg also frames the issue as extending beyond high-profile wealthy owners, noting that many residents with family properties are affected. Overall, the new tax is prompting controversy among homeowners while generating debate over fairness, implementation, and expected revenue outcomes.

Rhode Island’s ‘Taylor Swift Tax’ raises costs for owners of second homes

Rhode Island has enacted a new tax commonly referred to as a “Taylor Swift Tax,” aimed at raising revenue from non-primary residences. The law targets certain second homes that are not rented for at l...

- Rhode Island enacts a tax increase affecting certain non-primary residences, often described as a “Taylor Swift Tax.”

- The tax applies to second homes that are not rented for at least 183 days.

- Some owners of long-held family vacation properties report thousands of dollars in additional annual costs.

- Real estate groups and homeowners criticize aspects of transparency and question the measure’s fairness.

- Some affected families are considering legal challenges.

Rhode Island's new 'Taylor Swift Tax' is imposing thousands in extra annual costs on families owning long-held vacation homes, even modest ones. The law targets non-primary residences not rented for 183 days, impacting generations-old properties. Despite raising only a fraction of the state budget, many families face significant financial strain and are considering legal challenges, while real estate groups criticize the lack of transparency in its passage.

2 hours agoBloomberg News Boston money and power reporter Greg Ryan said that a Rhode Island tax increase on second homes is not just impacting the wealthiest residents like Taylor Swift, but that many residents with family properties worry about the impact on their finances. The Rhode Island tax comes as some other cities and states move to tax second homes at a higher rate, like the pied-a-terre tax proposed in New York City by Mayor Zohran Mamdani. (Source: Bloomberg)

10 hours ago

Naira trades with mixed but largely stable rates versus dollar and pound across Nigeria’s FX markets

Naira exchange rates against the US dollar and British pound show generally limited movement in Nigeria’s official and p...

Indian stock markets fluctuate as global cues and oil prices drive trade

Indian equity markets trade with sharp swings as investors react to global market sentiment and changes in oil prices. I...

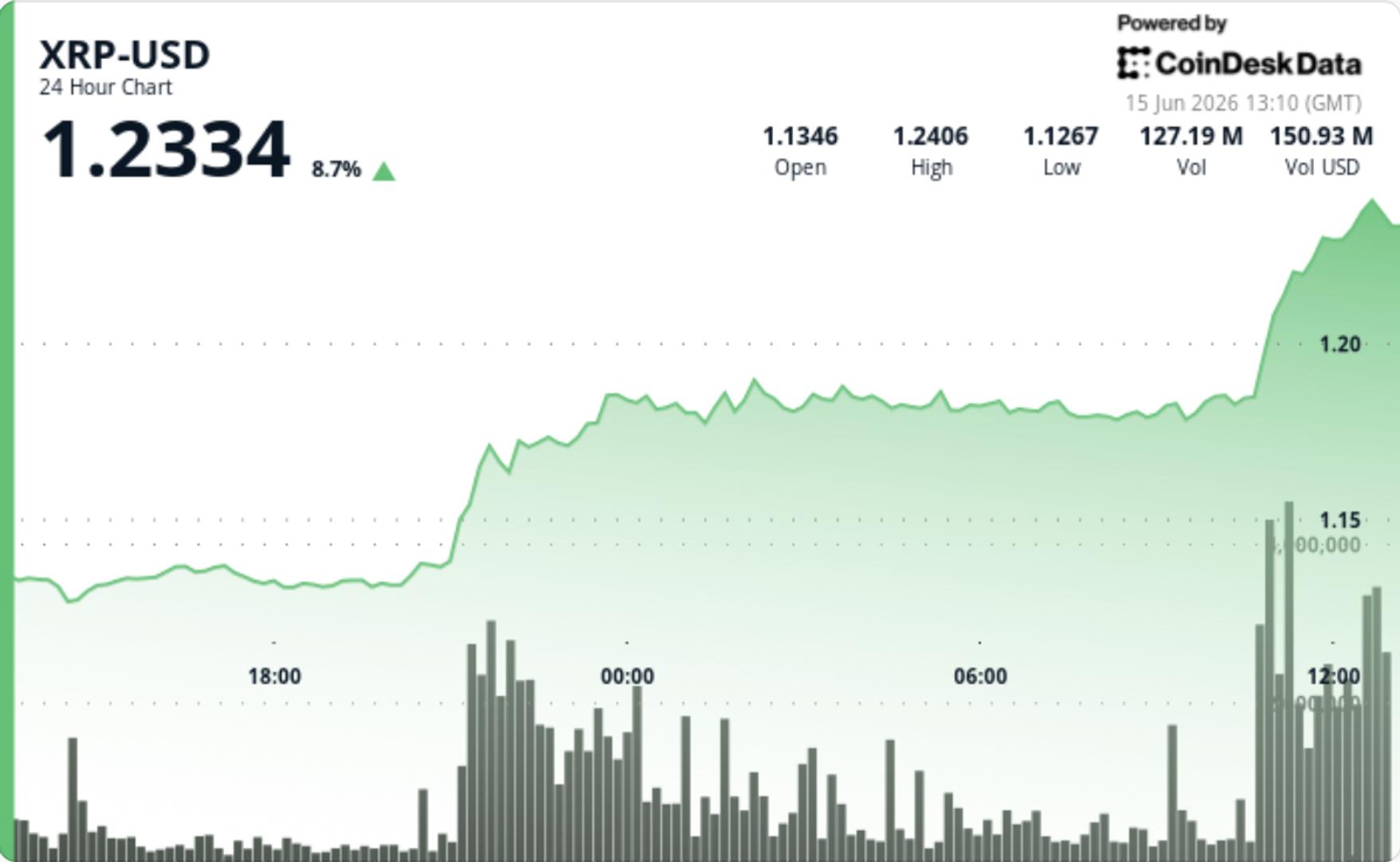

XRP trades around $1 as rallies face repeated selling and traders monitor key support

XRP is trading near the $1 area as multiple breakout attempts run into selling and traders watch several support and res...