Three outlets publish a personal-finance discussion asking whether people should delay retirement to pay for their daughter’s university fees. The articles focus on how different financial “levers” can improve long-term security, with all three emphasizing that extending working life typically has the greatest effect. The reasoning is that working longer can increase total income, potentially add to savings or retirement balances, and reduce the need to draw down assets earlier than planned. In turn, that may make it easier to fund education expenses without undermining future retirement outcomes. While the pieces center on the same question and reach the same broad conclusion about the impact of working longer, they present it as part of a broader consideration of household finances rather than a single prescriptive rule. Overall, they frame the decision as one of balancing near-term university costs against long-term retirement planning, noting that choices about timing, income, and retirement drawdowns are central to the outcome.

Articles weigh whether delaying retirement could help cover a daughter’s university costs

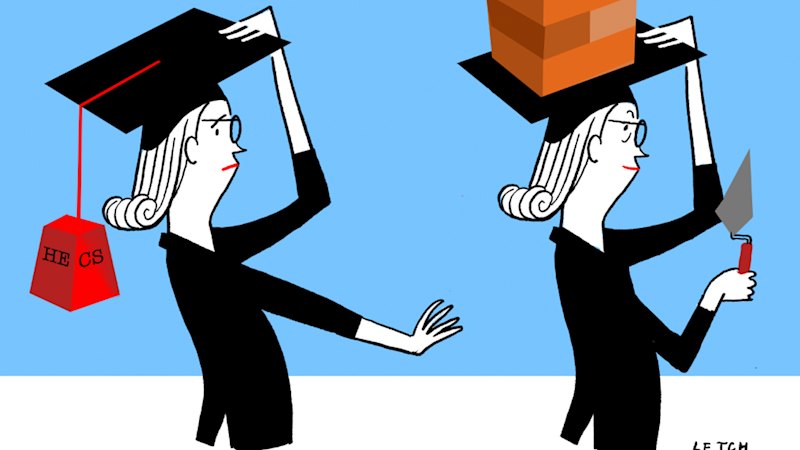

Three outlets publish a personal-finance discussion asking whether people should delay retirement to pay for their daughter’s university fees. The articles focus on how different financial “levers” ca...

- The articles discuss whether delaying retirement can help pay a daughter’s university fees.

- All sources state that working longer is typically the largest lever for improving long-term financial security.

- The focus is on balancing education costs with long-term retirement planning.

- The discussion compares different options that affect how households fund university expenses and manage retirement timelines.

Of the various levers we can pull to impact long term financial security, working longer typically has the largest impact.

6 hours agoOf the various levers we can pull to impact long term financial security, working longer typically has the largest impact.

6 hours agoOf the various levers we can pull to impact long term financial security, working longer typically has the largest impact.

6 hours agoNigeria petrol imports rise 207% in June as domestic supply declines

Nigeria’s petrol (fuel) imports increase sharply in June 2026, rising by 207% compared with the previous period, accordi...

Signed David Hockney print found in charity shop book sells for about £41,000

A signed David Hockney print discovered inside a charity shop book has sold for around £41,000, according to multiple re...

Multiple Porsche 911 models listed online, ranging from 1980s classics to 2018 Turbo S

A group of Porsche 911 listings highlighted across Bring a Trailer features a mix of classic and modern models available...